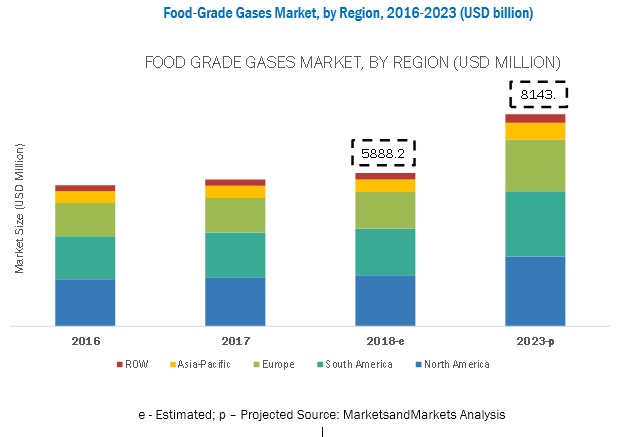

Food Grade Gases Market Projected to Reach $8.1 Billion by 2023

The report "Food Grade Gases Market by Type (Carbon Dioxide, Nitrogen, Oxygen), Application (Freezing & Chilling, Packaging, Carbonation), End-Use (Dairy & Frozen Products, Beverages, Meat, Poultry & Seafood), and Region - Global Forecast to 2023", The food-grade gases market is estimated to be valued at USD 5.9 billion in 2018 and is projected to reach USD 8.1 billion by 2023, at a CAGR of 6.7% from 2018 to 2023. Shifting consumer preferences toward convenient food packaging owing to their on-the-go lifestyles and the growing number of microbreweries across all regions are some of the factors driving the growth of the food-grade gases market.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=9473111

The freezing and chilling segment is projected to account for the largest share in the food-grade gases market

The food industry’s key challenges are to avoid microbial deterioration and increase the shelf life of products. One of the most effective methods of fighting these microbes is by chilling & freezing the products. When the temperature is lowered below the freezing point, the growth of micro-organisms decreases rapidly. Freezing slows down many enzymatic processes as well, thereby making food products more shelf stable. Chilling a food product reduces the risk of bacterial growth. The freezing and chilling of foods are essential to prevent spoilage. As manufacturers, consumers, and retailers demand these technologies, the use of food-grade gases is expected to increase.

Carbon dioxide segment has the highest share in the food grade gases market.

On the basis of type, carbon dioxide has the highest share. It is widely used for carbonation in soft drinks, beers, and other alcoholic drinks. The gas has applications in conserving wine, grape juices, and other juices. Beverage-grade carbon dioxide, which is considered an ingredient in the beverage industry, should be compliant with the strongest regulations of the EC (E290) and International Society of Beverages Technologists (ISBT). Carbon dioxide is also used for Modified Atmosphere Packaging (MAP); it is injected and frequently removed to eliminate oxygen from the package. Due to the advancement in packaging technologies, the demand for carbon dioxide is projected to remain the highest in the food-grade gases market.

Bulk segment is expected to show fastest growth during the forecast period

Based on the volume required by end-users, the gases are either supplied in bulk or cylinder. Companies that require large volumes of gases opt for bulk supplies for easy transportation and storage. On the other hand, companies that require lesser volumes of gases generally opt for gases in cylinders. Owing to the factors such as ease of handling, transportation, and storage, the bulk mode of supply is projected to register a higher CAGR during the forecast period.

Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=9473111

North America is projected to retain the largest market share during the forecast period.

North America accounts for a 33% share of the food-grade gases market. The large beverage industry and the rising trends of microbreweries create a huge demand for carbon dioxide in the North American region, with the US being the largest and fastest growing market. Also, because of the presence of highly organized retail chains and cold chain infrastructure, the North American region holds the largest market share in the food-grade gases market. Further, the increasing preferences for on-the-go meals than conventional home-cooked meals and the growing demand for bakery and confectionery have led to a significant increase in the demand for food-grade gases in North America.

This report includes a study on the marketing and development strategies, along with a study on the product portfolios of the leading companies. It includes the profiles of leading companies such as The Linde Group (Germany), Air Products & Chemicals (US), Air Liquide (France), The Messer Group (Germany), Taiyo Nippon Sanso (Japan), Wesfarmers Ltd. (Australia), SOL Group (Italy), Gulf Cryo (Kuwait), Air Water, Inc. (Japan), Massy Group (Caribbean), PT Aneka Industri (Indonesia), and The Tyczka Group (Germany).